Related Distributions

- If is a normal distribution, then

- If is distributed log-normally, then is a normal random variable.

- If are n independent log-normally distributed variables, and, then Y is also distributed log-normally:

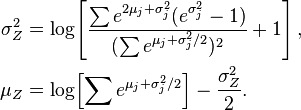

- Let be independent log-normally distributed variables with possibly varying σ and μ parameters, and . The distribution of Y has no closed-form expression, but can be reasonably approximated by another log-normal distribution Z at the right tail. Its probability density function at the neighborhood of 0 has been characterized and it does not resemble any log-normal distribution. A commonly used approximation (due to Fenton and Wilkinson) is obtained by matching the mean and variance:

In the case that all have the same variance parameter, these formulas simplify to

- If, then X + c is said to have a shifted log-normal distribution with support x ∈ (c, +∞). E = E + c, Var = Var.

- If, then

- If, then

- If then for

- Lognormal distribution is a special case of semi-bounded Johnson distribution

- If with, then (Suzuki distribution)

Read more about this topic: Log-normal Distribution

Famous quotes containing the word related:

“The question of place and climate is most closely related to the question of nutrition. Nobody is free to live everywhere; and whoever has to solve great problems that challenge all his strength actually has a very restricted choice in this matter. The influence of climate on our metabolism, its retardation, its acceleration, goes so far that a mistaken choice of place and climate can not only estrange a man from his task but can actually keep it from him: he never gets to see it.”

—Friedrich Nietzsche (1844–1900)

Related Phrases

Related Words