Triple Exponential Smoothing

Triple exponential smoothing takes into account seasonal changes as well as trends. It was first suggested by Holt's student, Peter Winters, in 1960. Suppose we have a sequence of observations {xt}, beginning at time t = 0 with a cycle of seasonal change of length L.

The method calculates a trend line for the data as well as seasonal indices that weight the values in the trend line based on where that time point falls in the cycle of length L.

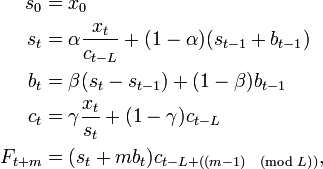

{st} represents the smoothed value of the constant part for time t. {bt} represents the sequence of best estimates of the linear trend that are superimposed on the seasonal changes. {ct} is the sequence of seasonal correction factors. ct is the expected proportion of the predicted trend at any time t mod L in the cycle that the observations take on. To initialize the seasonal indices ct-L there must be at least one complete cycle in the data.

The output of the algorithm is again written as Ft+m, an estimate of the value of x at time t+m, m>0 based on the raw data up to time t. Triple exponential smoothing is given by the formulas

where α is the data smoothing factor, 0 < α < 1, β is the trend smoothing factor, 0 < β < 1, and γ is the seasonal change smoothing factor, 0 < γ < 1.

The general formula for the initial trend estimate b0 is:

Setting the initial estimates for the seasonal indices ci for i = 1,2,...,L is a bit more involved. If N is the number of complete cycles present in your data, then:

where

Note that Aj is the average value of x in the jth cycle of your data.

Read more about this topic: Exponential Smoothing

Famous quotes containing the words triple and/or smoothing:

“And DANTE searched the triple spheres,

Moulding nature at his will,

So shaped, so colored, swift or still,

And, sculptor-like, his large design

Etched on Alp and Apennine.”

—Ralph Waldo Emerson (1803–1882)

“Generation on generation, your neck rubbed the windowsill

of the stall, smoothing the wood as the sea smooths glass.”

—Donald Hall (b. 1928)